Public Policy

Comcast and Time Warner Cable File Applications and Public Interest Statement with FCC

This morning, we’ve taken the next step in the process in our transaction with Time Warner Cable (TWC) by filing our joint Applications and Public Interest Statement with the FCC. Last week, we filed our Hart-Scott-Rodino notification with the Department of Justice, and tomorrow I’ll be testifying before the U.S. Senate Judiciary Committee. These requests for review to the FCC and the DOJ have begun the formal regulatory approval process for this transaction.

The FCC filing lays out in considerable detail how Comcast and TWC are better together for millions of customers and businesses, describing the exciting enhanced services and other concrete consumer benefits that will be available because of the transaction. Importantly, we show that these significant benefits are achieved without diminishing competition in video, broadband, phone, programming, advertising, and other markets.

First, let's look at the extensive benefits of this deal, particularly for customers in TWC areas. Together, Comcast and TWC will bring millions of consumers the next-generation of broadband Internet, video, voice, and related technologies. The scale created by this transaction will accelerate investments in R&D, innovation, and infrastructure. And by combining the companies’ technological developments and know-how, their geographic reach, and Comcast’s strong balance sheet and investment culture, the post-transaction company will improve the experience for customers today and forge ahead to meet future challenges and needs.

For consumers, this means:

Nowhere will these benefits be more important than in the broadband space. While TWC has upgraded its entire network to DOCSIS 3.0 and has plans to improve speeds and further digitize its network, Comcast has already transitioned to a fully digital network, stands ready to implement DOCSIS 3.1 (the next-generation broadband standard), and has rolled out some of the fastest Internet speeds and the largest Wi-Fi network in the nation. For example, Comcast has increased broadband speeds 12 times in 12 years as shown in the chart below. Today, our most popular broadband tier is 25 Mbps, while TWC’s is 15 Mbps. One third of Comcast’s customers today receive speeds of over 50 Mbps. And we offer speeds of up to 505 Mbps in an increasing number of markets. We’ve got the fastest in-home Wi-Fi and we’re marching toward 1 million Wi-Fi hotspots, while TWC has a much more limited number of hot spots with only 29,000. This transaction will accelerate network upgrades in the TWC markets and produce a more advanced broadband network.

On the video front, Comcast will bring our industry-leading X1, VOD, and online video options to TWC customers. Our X1 Platform is the future of TV with a state-of-the-art user interface and product features that revolutionize the viewing experience – enhanced search, voice control, and apps embedded in the television user experience. Comcast’s robust Xfinity On-Demand will be extended to TWC systems – today we have 50,000 programming choices on TVs, while TWC has only about 15,000-20,000. And on XfinityTV.com and the Xfinity TV Go app, we offer 300,000-plus streaming choices and 50 live streaming TV channels – viewable in and outside the home. We’ll also offer TWC’s customers electronic-sell-through of movies and TV shows to own – a service Comcast’s customers have used over 2 million times since launching just six months ago. We’re excited to bring these video innovations to TWC customers.

As another benefit for consumers, we’ll extend network neutrality protection to millions more broadband customers through our commitment to the FCC’s Open Internet rules. Today, Comcast is the only company in America that is legally bound by the FCC’s now vacated Open Internet rules. We’ll extend those protections to customers in TWC areas. The FCC is already working on rules that will eventually extend to all ISPs, but for the immediate future, one guaranteed way to bring millions of customers under the Open Internet rules is through this transaction.

We also have committed to bring our nationally acclaimed, low-income broadband adoption program, Internet Essentials, into TWC markets. Already, in less than three years, we’ve connected over 1.2 million low-income Americans to broadband in Comcast markets across the country. We can’t wait to bring it to TWC cities like LA, Dallas, Charlotte, and New York City, making this opportunity available to millions more families and helping reduce the unacceptable digital divide in the country.

In addition to the significant benefits that will result for individual consumers, business customers will benefit as well, which is important for economic development. Comcast and TWC have made some inroads into the business market, offering small- and medium-sized businesses innovative services and a better value proposition than was previously available to such customers from legacy providers – and provoking competitive responses by those incumbents – lower prices and better quality services. Each company has had some success (capturing maybe 10 to 15 percent of the SMB market), but its limited geographic scope has constrained its ability to offer truly meaningful competition to the established providers. The combined company’s greater geographic reach and its combined expertise and services will allow it to become a stronger competitor, offering businesses of all sizes better options, lower prices, higher quality, and enhanced services.

Here’s an example. Today, if you had a real estate business with offices in New York, Boston, and Washington, DC – Comcast and TWC couldn’t easily offer you a seamless business solution for these multiple locations. The same if you had BBQ restaurants in Houston, Dallas, and Austin, Texas. Or a tech startup on the West Coast with programmers in Portland, Seattle, the Bay Area, and Los Angeles. Competition in the business market has been long in coming, and we can take it to a larger scale that will promote economic development.

The transaction will also result in new options for advertisers. The combined company will have the scale to invest in the development and deployment of dynamic ad insertion and addressable technologies for use in VOD and other cable and online programming that will bring added value to programmers and advertisers. And the increased scale of the combined company should make such advanced advertising buys more attractive to advertisers looking for larger audiences. This, in turn, should encourage programmers to make additional popular content available on VOD and other platforms, to the benefit of consumers.

It’s understandable why any large merger will attract questions about competition and consolidation. But this particular transaction actually raises few competition concerns. The number one reason why is shown in the map below. Comcast and TWC do not compete against each other in any area, so there is no reduction in consumer choice in any market. Customers will still have the same number of video, broadband, or phone options before the deal as after it. Comcast will serve less than 30% of the multichannel video market after the transaction closes and we divest about 3 million customers.

The traditional boundaries between media, communications, and technology are obsolete. The competitive ecosystem in which we operate includes companies with national and even global– scale like AT&T, Verizon, DirecTV, DISH, Netflix, Amazon, Apple, Yahoo, Google, and Facebook – who are competing with each other and us in unprecedented ways. As the graphs below demonstrate, many of these companies are far larger than our combined company would be in market capitalization, annual revenues, and/or customers.

Today, Google competes as a network, video, and technology provider, and 8 out 9 of the next Google Fiber markets the company announced are in Comcast or TWC areas. Apple tablets are viewing platforms for cable services even while Apple offers an online video service, Apple TV, and explores development of an Apple set-top box. Microsoft just announced that it will feature ads on the Xbox One, creating a new video advertising platform. And just last week, Amazon announced its own set-top box while it continues to leverage its unequaled sales platform and family of competitive tablets to promote its burgeoning Prime Instant Video business.

The business reason for this transaction is to create the scale that will allow Comcast to make larger investments in R&D, innovation, and infrastructure to enable us to compete more effectively in this incredibly dynamic marketplace. Scale allows us to make the investments to launch a successful program like Internet Essentials, and invest in our broadband, video, and phone products.

When we have the scale to increase investment in more markets, our competitors will invest too. For example, Randall Stephenson, CEO of AT&T, said when our deal was announced that it "puts a heightened sense of urgency" on broadband providers to "very, very aggressively" invest capital in their networks and improve their services.

Some have expressed concern about the scale of the new company and the competitive implications. As noted above, because the companies don’t overlap or compete against each other today, consumers will not lose any choices in any markets. This makes this deal fundamentally different from other recently proposed mergers challenged by antitrust regulators such as AT&T/T-Mobile. Each of the markets in which the companies operate is fiercely competitive.

In the traditional multichannel video market, competition is fierce, with multiple providers in every market. Just since 2009 when the DC Circuit threw out the 30% horizontal ownership limit on cable for the second time, competition has accelerated. DirecTV and DISH are the #2 and #3 video companies in the US; and Verizon is #5. Since 2009, the two nationwide DBS providers have added another 1.7 million subscribers and the telco video providers have added 6.2 million subscribers, while traditional cable operators have lost 7.3 million video subscribers.

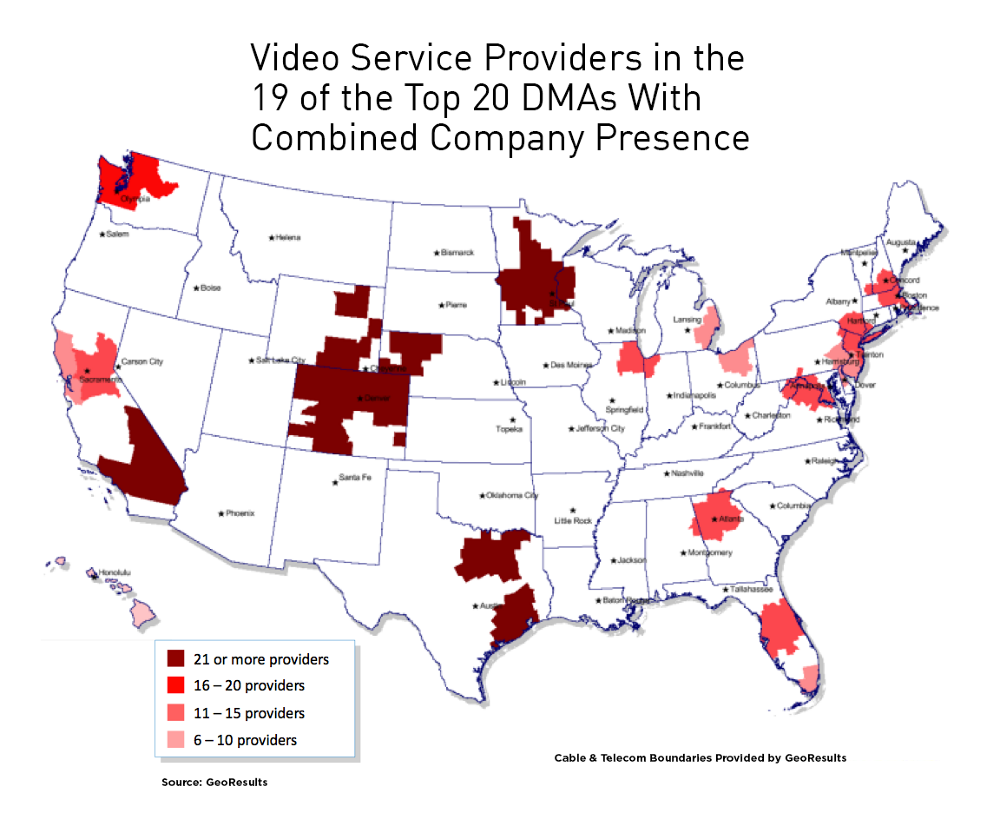

Thus, in each of the markets where Comcast or TWC compete, there is fierce competition for video, high speed data, and voice customers from multiple competitors. Indeed, while critics have tried to suggest that competition will be harmed somehow because the combined company will have a presence in 19 of the top 20 DMAs (a charge that ignores both that Comcast is already in 16 of those DMAs today and that DMAs are not "markets" for any relevant purpose in the review), the map and chart immediately below tell the competitive video and broadband reality at the DMA (or MSA level):

And this is just one dimension of the video competition that Comcast and TWC face, in a dynamic and increasingly mobile and global marketplace overflowing with innovation and consumer choice. Internet and device companies, with newfound global scale, also are competing aggressively in the video marketplace and in the larger broadband value circle. For example, Netflix now has over 33 million customers in the United States alone, with another 11 million international customers; Google’s video websites now attract over 157 million unique viewers each month who watch nearly 13 billion videos; Apple iTunes viewers purchase over 800,000 TV episodes and over 350,000 movies per day.

Turning to the broadband market, there has been a lot of focus on competition in broadband services. Our filing takes a detailed look at what’s really going on in today’s consumer marketplace. First of all, the chart below shows that in all of the top 20 metropolitan statistical areas (MSAs), there will be no change in the number of broadband competitors as a result of this transaction.

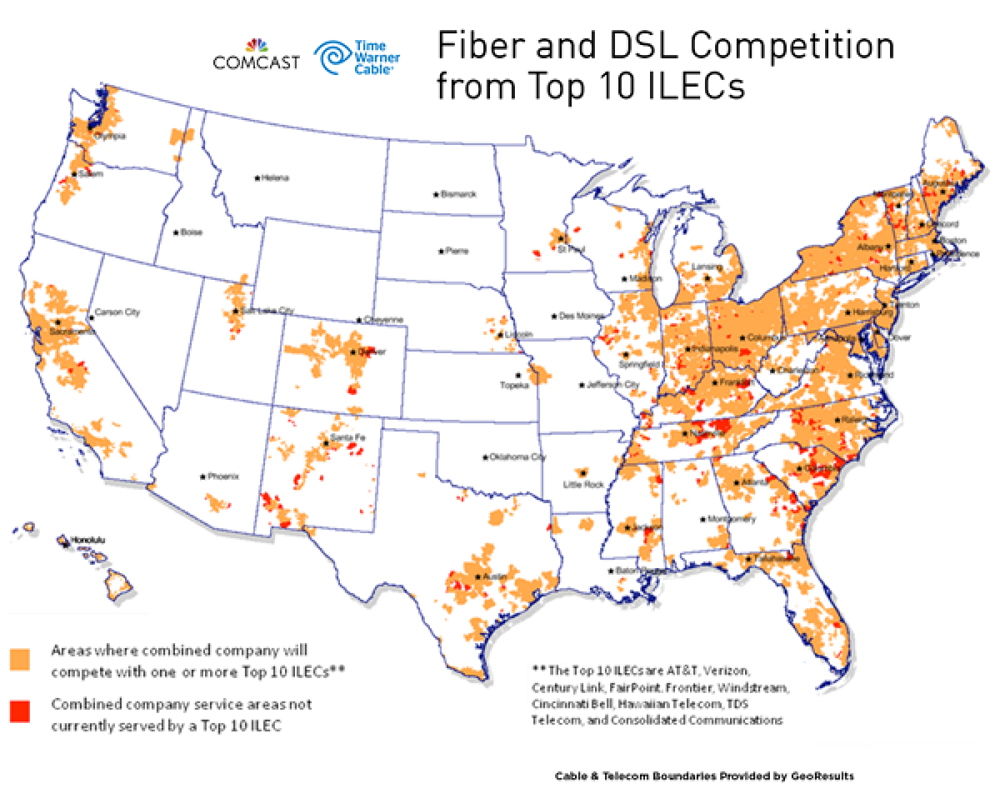

And as shown in the map below, in 98.4 percent of Comcast and TWC’s combined service areas, broadband customers have a choice between Comcast or TWC and one or more top-10 ILEC competitors. Only about 1.6% of customers are not served by a top-10 ILEC in addition to Comcast or TWC. Those ILECs offer various fiber and DLS based services. Contrary to the picture some have painted of DSL as a defunct service, between December 2008 and December 2012, DSL-based broadband connections grew at an average annual rate of 26%, exceeding cable broadband’s pace of growth of 18%. DSL providers offer speeds equal to or exceeding the FCC’s broadband speed threshold. For example, Verizon offers DSL service at speeds up to 15 Mbps, Frontier offers speeds up to 25 Mbps, and CenturyLink offers speeds up to 40 Mbps. AT&T offers speeds up to 45 Mbps through its DSL-based U-verse service and plans to offer speeds as high as 100 Mbps in the future. Companies are also investing in upgrading DSL service through new technologies such as VDSL2 and pair bonding.

Service areas shown represent areas in which the top-10 ILEC providers offer fiber and/or DSL-based Internet access service of any speed. Service area boundaries have been estimated using census block data, wire center locations, and other publicly available information.

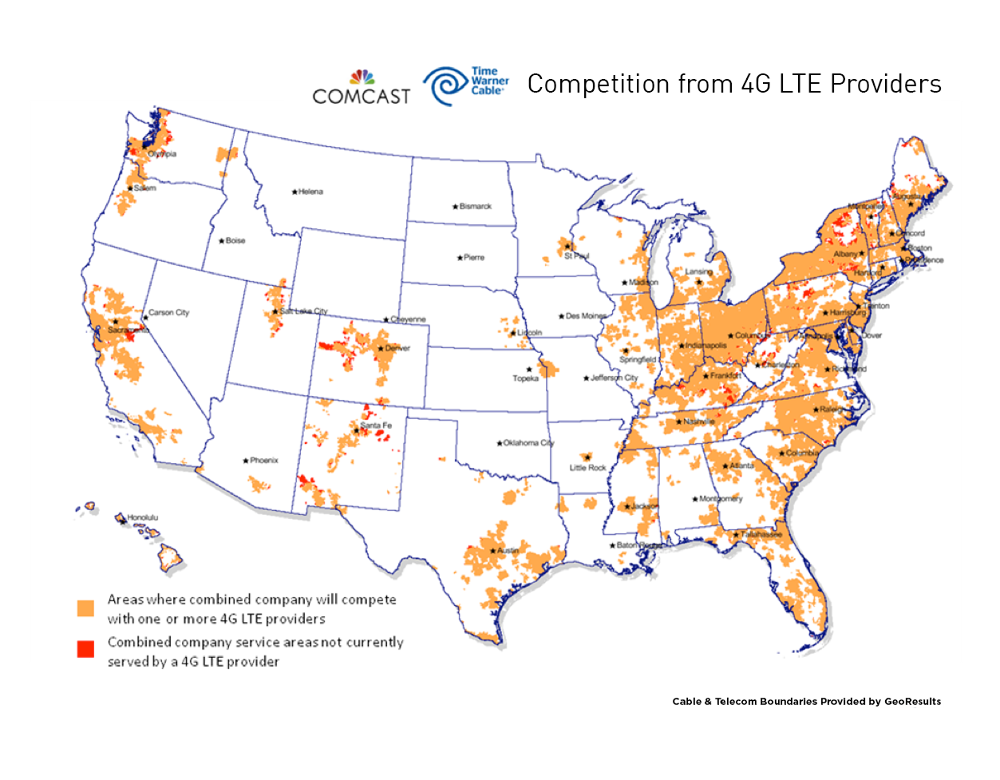

In addition to wired competition, wireless broadband is here today, already a meaningful broadband alternative, and becoming a more and more important competitor to wired broadband given the accelerating speed and reliability of advanced wireless networks, the growing value of mobility, and the fact that consumers increasingly use tablets and smartphones as "first screens." This reality was reinforced when President Obama enlisted two wireless providers to help him achieve his goal of bringing ultra-high speed Internet connections to schools and making broadband available to students at school, in the community, and at home. The map below shows 4G deployment today in Comcast and TWC areas – and you can see it overlaps nearly every market.

Wireless 4G technology can deliver speeds well over 50 Mbps and averaging in the double digits. While pricing for wireless broadband plans with substantial bandwidth is higher today than other broadband services, these prices have and will continue to come down over time as wireless providers achieve more bandwidth. And for many lighter broadband users, that’s not even an issue today.

Concerns about control of programming should also not raise substantial competition concerns. TWC adds relatively little programming to the combined company. As a distributor of programming, Comcast has good relationships with programmers across all categories. With broadcasters, Comcast has never lost a signal in a retransmission consent dispute. Discovery Communications CEO David Zaslav recently said "Comcast is a great company." We’ve been a friend to independent programmers (160 of the channels carried on Comcast Cable systems are independent), expanding carriage of independent channels, launching new independent linear channels, and featuring independent movies on demand. We’ll carry these values into our dealings with programmers going forward.

Comcast will have less than a 30% share of the national market of video subscribers nationwide, a level the courts have repeatedly found does not give rise to concerns. Comcast doesn’t own the overwhelming majority of programming it distributes, with more than 6 out of every 7 channels carried not owned by the company. Since the close of the NBCUniversal transaction, we’ve launched several new independent networks, including BBC World News, ASPiRE, Baby First Americas, Revolt, and El Rey.

Last year, Comcast celebrated its 50th anniversary. Founded as a small company in Tupelo, MS, we’ve grown through five decades to become a cutting-edge media and technology company that employs 136,000 people across the country and beyond. We’ve grown organically and through acquisitions, from a one-product company showing a few broadcast channels, to a multi-product company offering consumers nearly unlimited choices today. We’ve invested to help build a robust broadband network – and we’ve been an industry leader in product innovation.

Along the way, we’ve kept the promises we’ve made in bringing benefits to consumers from our transactions. We’ve met or exceeded our commitments in every deal. Our most recent, the NBCUniversal transaction, contained more than 150 conditions. We’ve demonstrated over and over again in our annual compliance reports that we’ve met or exceeded these conditions. In over three years, we had only one instance where the FCC took issue with the company’s compliance, which was fully addressed. We promised to expand our broadband network by 4,500 miles, and we exceeded that promise and built 6,300 miles. We promised to add 300,000 new homes passed by broadband, and we more than doubled that and added 715,000 homes. We promised to expand broadband to six additional communities, and we expanded to 33. With Internet Essentials, we continually upgraded and expanded the program which was originally set to expire this year, and recently announced we would extend it indefinitely. We are proud of our record of honoring our commitments.

Time and time again, Comcast has delivered – and over-delivered – on its promises to unleash more investment and innovation. Together with TWC, we are fully poised to do so again.

We look forward to working with the FCC and the DOJ during the review process. We expect a rigorous review as we’ve had in our previous deals, and believe an objective weighing of the significant public interest benefits that are offered by this transaction and the lack of competitive concerns should lead to approval.

Important Information For Investors And Shareholders

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. In connection with the proposed transaction between Comcast Corporation ("Comcast") and Time Warner Cable Inc. ("Time Warner Cable"), on March 20, 2014, Comcast filed with the Securities and Exchange Commission (the "SEC") a registration statement on Form S-4 containing a preliminary joint proxy statement of Comcast and Time Warner Cable that also constitutes a preliminary prospectus of Comcast. The registration statement has not yet become effective. After the registration statement is declared effective by the SEC, a definitive joint proxy statement/prospectus will be mailed to shareholders of Comcast and Time Warner Cable. INVESTORS AND SECURITY HOLDERS OF COMCAST AND TIME WARNER CABLE ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS AND OTHER DOCUMENTS FILED OR THAT WILL BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain free copies of the registration statement and the joint proxy statement/prospectus and other documents filed with the SEC by Comcast or Time Warner Cable through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Comcast are available free of charge on Comcast’s website at http://cmcsa.com or by contacting Comcast’s Investor Relations Department at 866-281-2100. Copies of the documents filed with the SEC by Time Warner Cable will be available free of charge on Time Warner Cable’s website at http://ir.timewarnercable.com or by contacting Time Warner Cable’s Investor Relations Department at 877-446-3689.

Comcast, Time Warner Cable, their respective directors and certain of their respective executive officers may be considered participants in the solicitation of proxies in connection with the proposed transaction. Information about the directors and executive officers of Time Warner Cable is set forth in its Annual Report on Form 10-K for the year ended December 31, 2013, which was filed with the SEC on February 18, 2014, its proxy statement for its 2013 annual meeting of stockholders, which was filed with the SEC on April 4, 2013, and its Current Reports on Form 8-K filed with the SEC on April 30, 2013, July 29, 2013 and December 6, 2013. Information about the directors and executive officers of Comcast is set forth in its Annual Report on Form 10-K for the year ended December 31, 2013, which was filed with the SEC on February 12, 2014, its proxy statement for its 2013 annual meeting of stockholders, which was filed with the SEC on April 5, 2013, and its Current Reports on Form 8-K filed with the SEC on July 24, 2013, August 16, 2013 and February 14, 2014. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the participants in the proxy solicitations and a description of their direct and indirect interests, by security holdings or otherwise, are contained in the preliminary joint proxy statement/prospectus filed with the SEC and will be contained in the definitive joint proxy statement/prospectus and other relevant materials to be filed with the SEC when they become available.

Cautionary Statement Regarding Forward-Looking Statements

Certain statements in this communication regarding the proposed acquisition of Time Warner Cable by Comcast, including any statements regarding the expected timetable for completing the transaction, benefits and synergies of the transaction, future opportunities for the combined company and products, and any other statements regarding Comcast’s and Time Warner Cable’s future expectations, beliefs, plans, objectives, financial conditions, assumptions or future events or performance that are not historical facts are "forward-looking" statements made within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements are often, but not always, made through the use of words or phrases such as "may", "believe," "anticipate," "could", "should," "intend," "plan," "will," "expect(s)," "estimate(s)," "project(s)," "forecast(s)", "positioned," "strategy," "outlook" and similar expressions. All such forward-looking statements involve estimates and assumptions that are subject to risks, uncertainties and other factors that could cause actual results to differ materially from the results expressed in the statements. Among the key factors that could cause actual results to differ materially from those projected in the forward-looking statements are the following: the timing to consummate the proposed transaction; the risk that a condition to closing of the proposed transaction may not be satisfied; the risk that a regulatory approval that may be required for the proposed transaction is not obtained or is obtained subject to conditions that are not anticipated; Comcast’s ability to achieve the synergies and value creation contemplated by the proposed transaction; Comcast’s ability to promptly, efficiently and effectively integrate Time Warner Cable’s operations into those of Comcast; and the diversion of management time on transaction-related issues. Additional information concerning these and other factors can be found in Comcast’s and Time Warner Cable’s respective filings with the SEC, including Comcast’s and Time Warner Cable’s most recent Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Comcast and Time Warner Cable assume no obligation to update any forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date hereof.